Private investment in education has grown up. What used to be a sector driven by mission and modest margins is now attracting institutional capital, sophisticated deal structures, and investors who know what they want. One structure you'll encounter repeatedly in large-scale school development is the PropCo/OpCo model — and if you're on either side of a school transaction, you need to understand it.

What PropCo/OpCo Actually Means

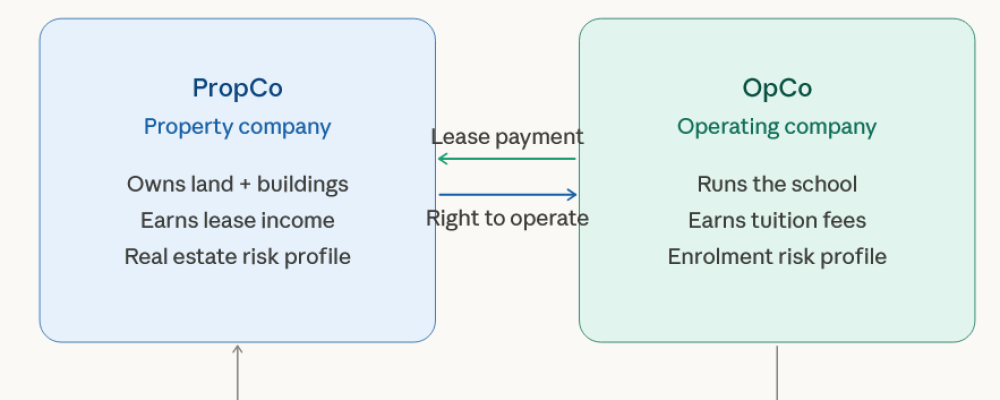

The concept is straightforward, even if the legal execution isn't. You split the school project into two separate legal entities.

The Property Company — PropCo — owns the land, buildings, and infrastructure. It generates returns through rental income paid by the school operator. Its risk profile looks more like real estate than education, which means it attracts a different type of investor.

The Operating Company — OpCo — manages the school. Academic delivery, staffing, admissions, regulatory compliance, and parent relations — all of it is handled here. Revenue comes from tuition fees. Risk is directly linked to enrolment performance, leadership quality, and educational reputation.

The two entities are linked through a long-term lease. The OpCo pays rent to the PropCo in return for the right to operate from the property. That lease forms the structural backbone of the entire arrangement.

Why the Separation Matters

Real estate investors and education operators view risk and return differently. Combining them in the same entity causes misalignment. Separating them enables each to be capitalized on, governed, and exited according to its own terms.

For the PropCo investor, the appeal is an infrastructure-style return — steady lease income from a creditworthy operating tenant, with long-term asset appreciation. They don't need to understand curriculum frameworks. They need to understand the quality and resilience of the OpCo.

For the OpCo operator, removing property ownership from the operational balance sheet is a valuable advantage. Capital that would otherwise be tied up in bricks and mortar can be redirected toward hiring excellent teachers, marketing to prospective families, and building the school's reputation — the factors that truly influence enrolment.

For institutional investors assessing the whole project, separation provides the financial transparency they need. Real estate and school performance can be evaluated separately. That clarity is important when you're aiming to attract serious capital.

Where Projects Go Wrong

I've observed the same structural mistakes repeat across school development projects in multiple markets.

The most damaging mistake is setting lease payments without a realistic reference to early enrolment projections. A lease that appears sustainable at full capacity can choke a school in its first three years — before it has had time to build a reputation and fill seats. The financial model must be stress-tested against conservative projections over a five- to ten-year horizon, not just at stabilized occupancy.

The second recurring issue is misaligned expectations between PropCo and OpCo investors. Property investors expect stable returns from the start, while education investors recognize that schools typically take 3 to 5 years to become financially mature. When both types of investors sit at the same table without a clear understanding of each entity's return timeline, conflict is likely to occur.

A third concern — often overlooked — is governance. Keeping the two entities legally and operationally separate isn't just good practice; it's essential for attracting institutional capital. Shared directors, undocumented intercompany arrangements, or commingled accounts create legal risks that become significant the moment either party wishes to exit or restructure.

What This Means If You Own or Are Acquiring a School

The PropCo/OpCo structure isn't suitable for every project. Smaller transactions don't require the additional legal complexity and governance overhead. However, when a project is sufficiently large to warrant separate capitalization of the real estate and operational elements — or when the investor group includes parties with genuinely different risk appetites — the structure justifies its complexity.

From an advisory perspective, the valuation implications are substantial. Whether you're a school owner contemplating a sale, a developer designing a new project, or a buyer assessing an acquisition, understanding how the PropCo and OpCo interact influences how you model cash flows, structure the deal, and ultimately determine the asset's worth.

At Halladay Education Group, we collaborate with school owners and discerning buyers navigating these decisions throughout Canada, the US, and the UK. Our advisory focus is on the sell side — assisting school owners in understanding the value of their creations and positioning them effectively for the right transaction.

If you own a private school and are considering your next move — whether that's a full sale, a recapitalization, or simply gauging your school's value in today's market — I invite a confidential conversation.

Contact us at info@halladayeducationgroup.com or 1-800-687-1492—no pressure, no obligation — just an honest conversation with someone who knows this market.