How Is a Private School Actually Valued? The Formula Buyers Use

If you have ever asked an advisor what your school is worth and gotten a vague answer, here is the direct version. Buyers value a school by taking its adjusted EBITDA and multiplying it by a number that reflects size, risk, and growth. That is the entire mechanic. The complexity, and the place where owners either gain or lose real money, is in how each of those three inputs actually gets calculated.

The question I get asked most often is not "what is my school worth?" It is "just give me a rough number, so I know whether this is even worth pursuing." I understand the instinct. I also know that a rough number handed out before anyone has looked at your sector, your enrollment trend, or your real estate position is worse than no number at all. Owners anchor on it, then feel shortchanged or oversold when the real figure lands somewhere else entirely.

What formula do buyers actually use?

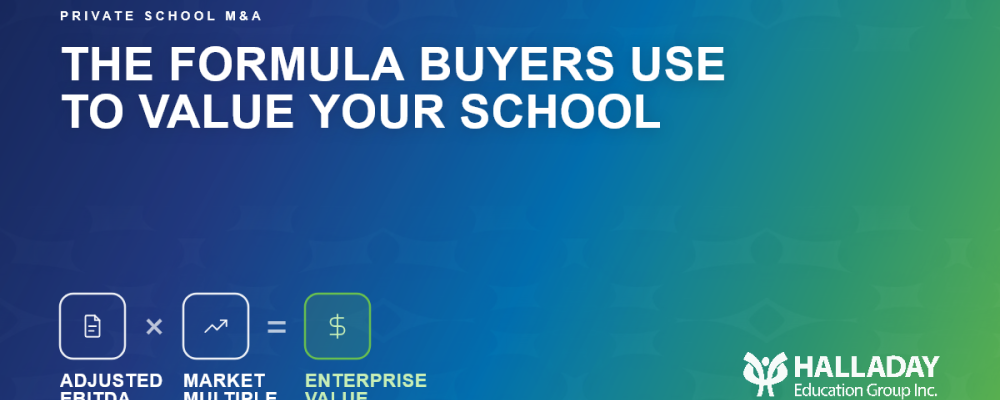

The core calculation is simple: enterprise value equals adjusted EBITDA multiplied by a multiple. EBITDA stands for earnings before interest, taxes, depreciation, and amortization, and it is the standard proxy buyers use for the real cash-generating power of your school.

The word that matters most in that sentence is "adjusted." Nobody pays a multiple on your raw bottom line. They pay a multiple on a normalized number that strips out anything that is not a true, recurring cost of running the school.

Why does "adjusted" EBITDA matter so much?

Because this is where price gets made or lost. Adjusted EBITDA adds back personal expenses run through the school, one-time legal or repair costs, above-market owner compensation, and any other item that would not exist under new ownership. Done properly, these add-backs can move your valuation by hundreds of thousands of dollars. If done poorly or without documentation, a buyer's accountants will refuse to credit them, and your number will come up during diligence.

This is also exactly where deals unravel after the letter of intent. I have written before about how quality of earnings problems are the single most common reason school sales collapse in the 90 days after an LOI is signed. The fix is the same one that protects your valuation in the first place: clean, reviewed financials with every add-back documented and receipted, well before a buyer ever sees your numbers.

Why is there no single multiple for a private school?

This is the question every owner asks, and the honest answer is that anyone who hands you one universal number is guessing. The multiple is not a single figure. It moves on at least ten variables at once, and generic industry ranges mislead owners precisely because they collapse all of those variables into one.

Sector is the first split. Early childhood education, PreK-12, ESL and language institutes, career colleges, and universities each have their own buyer pools, funding models, and risk profiles. A multiple that fits one sector rarely transfers cleanly to another.

Geography is the second. A school in the same sector, with the same EBITDA, prices differently in Canada than in the United States, and both differ again from Europe, MENA, and South America, where regulatory frameworks, currency risk, and buyer depth all shift the number in different directions.

Program mix matters within a single school. A premium K-12 campus with real tuition pricing power is not valued the same way as a healthcare career college program tied to licensure and government funding eligibility, even if the two schools post identical earnings this year.

Even holding sector, geography, and program constant, the multiple still moves on:

- The scale of adjusted EBITDA and its direction. A school earning $2 million and a school earning $10 million in the same sector rarely trade on the same multiple, and a school trending upward commands more than one trending flat or down at the same size.

- Whether turnkey management is in place, so the school runs without the owner in the room.

- Whether the school carries high-value assets, such as owned real estate or expensive specialized equipment, which can pull the entire valuation conversation toward asset value rather than earnings alone.

- How prohibitive the regulatory or licensing barriers to entry are in that jurisdiction, which determines how much competitive protection a buyer is actually purchasing along with the school.

- Local supply and demand, for enrollment and for comparable schools currently on the market.

- How heavy the change-of-control requirements are with the relevant regulator or accreditor. A slow or uncertain approval process gets priced as risk, no matter how strong the underlying school is.

- Buyer inventory, meaning how many qualified buyers are actively looking for that specific type of school in that specific market right now.

That is ten variables interacting before anyone applies a multiple to a single dollar of EBITDA. This is exactly why I treat any generic published range, including ranges I could quote from industry data, as a starting orientation at best and never as an answer for a specific school.

What does this look like in the market right now?

A few patterns I am seeing in active deals, to make the variables above concrete rather than abstract:

- Premium K-12 private schools in strong US and Canadian markets with adjusted EBITDA in the $2 million to $5 million range are commanding higher multiples than that profile received a few years ago, because buyer demand for scale-ready platforms at that size is intense right now.

- Healthcare-focused career colleges, especially nursing programs, are priced higher in Canada than in the US, largely due to stronger domestic student demand and more stable program funding north of the border.

- ESL and language institute multiples are under pressure as the US international student market softens, and buyers are pricing that headwind into offers even for schools with strong current enrollment.

- ECE multiples are moving in opposite directions depending on the border. In the US, consolidation is concentrating ownership and pushing multiples up. In Canada, the ECE market remains fragmented, and that fragmentation is holding multiples down.

- Strategic buyers, meaning operators who can extract real synergies from the acquisition, typically pay more than financial buyers underwriting the school as a standalone investment.

- A school with genuine year-on-year growth can command a stronger outcome, sometimes structured with an earn-up rather than a flat price, rewarding the seller if that growth continues after closing.

None of this is a table you can look up once and rely on. It is a live picture that shifts by sector, by border, and by quarter, which is exactly why the number that matters has to come from someone actively tracking these patterns, not from a published range.

How does real estate change the math?

If you own your campus, do not let it get buried inside your operating EBITDA. Real estate and school operations are frequently valued through different lenses, and how they interact depends on the same variables above, particularly asset value and local supply and demand. I have written a full explainer on how this separation can work in practice in my piece on PropCo/OpCo structures. Owners who blend the two in their thinking routinely leave value on the table, either overvaluing the operation, undervaluing the land, or overlooking a structure that would have served them better.

What can you actually control before you go to market?

You cannot change your sector, your geography, or the regulatory environment in which you operate. But several of the highest-leverage inputs into your multiple are entirely within your control, starting well before a buyer ever appears:

Owner dependence. A school that runs on the founder's personal relationships and daily involvement gets discounted, sometimes heavily, because the buyer is pricing the risk that performance drops the day you leave. I have written separately about how significant this discount can be and what to do about it.

Enrollment trend, not just enrollment level. Three years of stable or growing enrollment strengthen your position regardless of sector. A flat or declining trend works against you even if this year's numbers look fine, because buyers are pricing the next five years, not the last one.

Documentation quality. A clean data room, reconciled financials, and a well-organized add-back schedule do not just speed up diligence. They directly support the multiple a buyer is willing to underwrite, because every unanswered question gets priced as risk.

Regulatory and accreditation standing. Any pending issue, disclosed early and clearly, does far less damage than the same issue discovered by a buyer's team mid-diligence.

Frequently asked questions

Is the EBITDA multiple the only way to value a school? It is the most common method for established, profitable schools, but a discounted cash flow analysis is sometimes used alongside it, particularly for schools with newer campuses or rapidly changing enrollment where trailing EBITDA does not tell the full story.

Should I calculate my own adjusted EBITDA before talking to an advisor? It is useful groundwork, but most owners under-document their add-backs or miss ones a buyer would actually accept. A proper valuation conversation will identify which adjustments hold up and which do not.

Does a higher multiple always mean a better deal? No. Structure matters as much as the headline number. A higher multiple attached to a long earnout or heavy seller financing can be worth less than a lower multiple paid mostly in cash at closing.

Is there at least a rough multiple range I should expect, or a place to find out what mine would be? Be cautious of any range offered before someone asks about your sector, geography, program mix, EBITDA trend, asset base, regulatory environment, and buyer inventory. Those variables interact enough that a range accurate for one school can be meaningfully wrong for another in the same city. The only reliable number comes from a real conversation about your specific situation, not a published table.

Want to know what your school is actually worth?

The formula is simple. Applying it to your specific school is not, because sector, geography, program mix, asset base, and a half dozen other variables all move the number in different directions at once. That is exactly why a generic answer is worth very little, and a real one is worth a great deal. If you are considering a sale in the next one to three years, a confidential conversation now costs nothing and gives you a real answer instead of a guess.

Reach us at info@halladayeducationgroup.com and 1.800.687.1492.